The economic hangover of COVID-19: how long will it last?

As the Australian economy begins to emerge from hibernation, the question of what the recovery will look like – and how long it will take – is being hotly debated.

AMP Capital chief economist Dr Shane Oliver says that although economic activity is unlikely to return to pre-COVID-19 (coronavirus) levels until late in 2021, just a few months ago we were questioning whether the shutdowns would stop the spread of the virus and, if not, whether there would be a recovery at all.

Below he shares his predictions for some of Australia’s key economic measures and the risks to watch out for on the road back.

Economic growth

As measured by gross domestic product (GDP), economic growth in Australia has contracted and I expect and predict a very large hit to GDP – down about 10% – in the three months to June, with April’s retail sales figures recording the worst fall ever due to the COVID-19 restrictions and closures during this time.

The good news is that the shutdowns have been much shorter than the six months initially forecast by the Prime Minister, and now that they’re beginning to ease restrictions, GDP should recover from June onwards.

But the recovery won’t be fast – rather than a sharp rebound (or ‘V’ shaped recovery) I expect and project more of a ‘U’ shaped recovery – because while some parts of the economy will recover quickly, others will take longer. This is the sort of recovery that was experienced around the world following the global financial crisis.

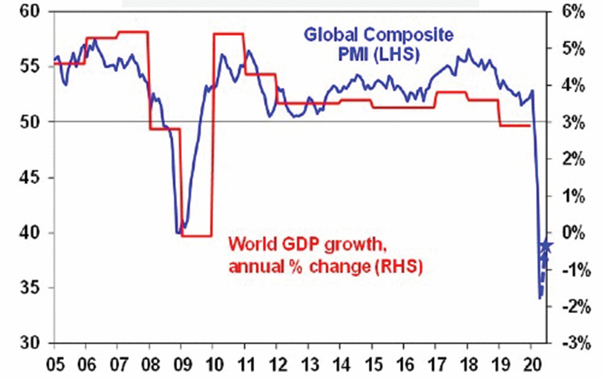

And globally, the fall in GDP is likely to be the biggest since the Great Depression of the 1930s. The blue line below, which tracks business confidence, shows how big the fall in global GDP could be, although it also shows that business confidence is beginning to pick up.

Global Composite PMI vs World GDP

Source: Bloomberg, AMP Capital

Inflation and interest rates

Inflation – which is currently around 1.9% in Australia – is expected to remain low, which should make it easy for the Reserve Bank of Australia to keep interest rates low. I think interest rates will remain at their current levels of around 0.25% for at least the next three years, which is good news for people with mortgages, and also for the economy, as people with home loans are one of the groups that spend the most.

Unemployment

If the Australian Government hadn’t introduced the JobKeeper assistance scheme, the unemployment rate in Australia today would probably be close to 15%. But thanks to this assistance it’s only 6% currently and I think it’s possible it may not even reach 8%, providing the economic recovery continues.

The share market

At the peak of the crisis, the Australian share market fell by almost 37%, but since then it’s recovered up by around 29%. And although dividend yields have been cut, they’re still more attractive than bank deposits due to low interest rates. It’s difficult to predict where the share market will go in the short term – more falls could occur as the market responds to bad news such as a drop in company profits. But over 12 to 24 months, share markets should rise.

House prices

There’s been a significant fall in the number of houses for sale and thanks to that we haven’t seen much of a fall in prices yet, but house prices are likely to fall if people are forced to sell as unemployment rises and as immigration falls. Sydney and Melbourne could also suffer from a lack of immigration-driven demand. I think prices on average could drop by about 10% which would take them to their mid-2019 levels. However, low interest rates continue to benefit the housing market.

The Australian dollar

I think we saw the low point for the Australian dollar against the US dollar at around 55c in March and it will probably move slowly higher as our economy recovers as it is expected to recover faster than the US economy.

The budget deficit

To support our economy, I think the Australian Government had to provide stimulus, and has done so in a way that’s affordable. Despite the assistance packages released by our government, the level of public debt in Australia is quite small compared to other economies.

Risks to look out for

Despite a fairly positive outlook, there are some risks on the horizon including:

• A second wave of infections

A second wave of infections could lead to a second wave of shutdowns, which would slow the economic recovery.

• The end of government stimulus

In late September when the JobKeeper assistance payments end and the JobSeeker payment for those looking for work is halved back to its pre-COVID-19 level, unemployment, bankruptcies and business closures could all rise, which would have impacts on consumer spending, house prices, economic growth and the share market.

• US/China tensions

COVID-19 has re-ignited tensions between the US and China and I expect this will continue in the run up to the US election in November. History tells us that US presidents don’t get re-elected when unemployment is rising or when the economy is in recession, so President Trump is trying to shift blame to China for political gain, which could drive volatility in investment markets. Australia’s current trade tensions with China are also a risk, but as long as they don’t escalate, we are still well placed to benefit from the Chinese economic recovery.

To sum it all up, while it will take a little while – and a little luck – I think the Australian economy is in a stronger position for a faster recovery than many other countries, mainly thanks to our good health outcomes and the strength of our government assistance.

©AMP Life Limited. First published June 2020